Thermally modified wood (TM) wood products have been available in the United States since Westwood Corp started exhibiting thermal-treated wood products at fairs, and companies such as Jartek Inc. and Stellac Inc, started to produce TM wood products (Sandberg et al., 2016). Initially, the production of TM wood products was intended as an alternative to substitute chromate copper arsenate treatments. Since the United States started creating restrictions regarding the use of toxic substances on their wood products many companies have begun to incorporate the production of TM wood products. According to Sandberg (2016) by 2012 there were already ten manufacturers across the US working producing thermally modified lumber.

The goal of this study was to evaluate the variability of the physical and mechanical properties of two thermally treated species currently manufactured in North America. One of the limitations that TM wood is facing is the lack of domestic manufacturers currently producing this product and the use of different equipment and treatments (schedules) which may create variability in final product performance.

TW treated yellow poplar (Liriodendron tulipifera) and red maple (Acer rubrum) were acquired from three different commercial sources in North America to conduct bending and strength (MOE/MOR) tests by following the ASTM D143 standard. Each company provided 14 samples from each species. Samples were conditioned at 20°C and relative humidity of 65% until they reached an equilibrium of moisture content before testing. ANOVA was then used to determine and compare the variability within and between each companies’ processes.

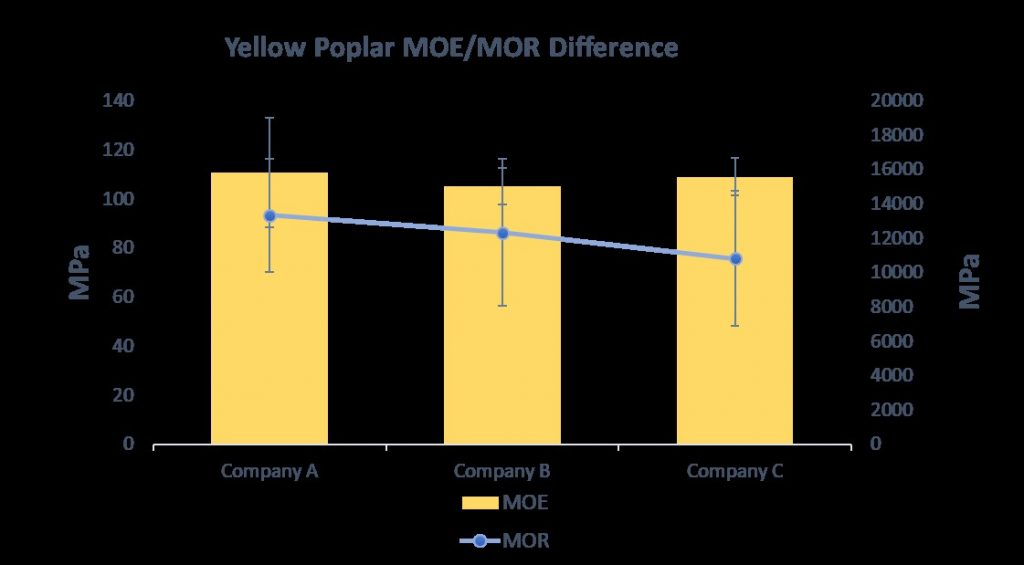

Figure 1. Yellow Poplar MOE/MOR Difference

Figure 1 shows a graph with the results obtained for both MOE and MOR for yellow poplar. The chart shows how similar the results from the three companies were. After running an ANOVA, the results displayed with 95% confidence intervals have they have equal means with a P-Values of 0.089 and 0.655 respectively.

Table 1. Red Maple MOE/MOR results.

Factor

N

Mean (MPa)

Standard Deviation

Group

MOE A

14

18,282

3,198

A

MOE B

14

17,352

1,075

A B

MOE C

14

16,310

1,100

B

The MOE/MOR values across the three companies share the mean with 95% confidence intervals and P-Values of 0.089 and 0.05. But Tukey’s comparison method displays that the MOE values from company B and C are different, and A shares the values between them. Statistically they might be different, but percentage-wise for the industry the difference is not that big.

Bibliography

Sandberg, D., & Kutnar, A. (2016). Thermally modified timber: recent developments in Europe and North America. Wood and Fiber Science, 48(1), 28-39.

UNECE/FAO. (2013). UNECE/FAO Forest Products Annual Market Review, United Nations Economic Commission for Europe, Food and Agriculture Organization of the United Nations, New York, and Geneva.

Innovation has been the key the in the past decades to develop products, process and services more effective, efficient and attractive to potential customers all across different practices/sectors including manufacturing, services and academia. Forest products are always evolving and creating innovative practices to satisfy customer needs and surpass expectations.

Figure 1. Thermally modified wood samples

The hardwood lumber market has decreased in the past 20 years, especially on 2009, where the great recession took place and since then there has been an emergence of innovative products that have caught the attention of the manufactures to start developing on their own practices (Buehlmann et al 2010 and Quesada et al., 2006). One of the innovative products that has started to caught the US lumber market is the thermally modified (TM) lumber with the large variety of exterior and interior applications, including musical instruments, guns stocks, decking applications, outdoor furniture, siding, roofing, door and window frames, flooring and interior furniture. With these applications, new opportunities have been brought to use low value timber, since there is a wide availability of timber in both private and public lands that are considered low-value timber (lower value species, quality, size) (Baynes, Herbohn and Gregorio, 2014).

Thermally-modified (TM) wood has been available since early 1990s in Europe where it was developed as an alternative to tropical hardwoods. Consumers, such as architects, engineers and contractors has started questioning; what are the performances of TM wood? how expensive the product is compare to similar lumber products? does it use any preservatives that could imply hazardous to the environment? Due to how new the product is to the U.S., consumers are still hesitant about its use (Wardell 2015). Even though there is a variety of information on the Internet, magazines and publications regarding the performance of the TM wood, there is still a low level of awareness of TM wood products (Espinoza et al, 2015). According to Boonstra (2008) due the increased demand on sustainable building materials and the restrictive regulations regarding the use of toxic chemicals; the interest on thermal treatments has started to grow, due to its lack of preservatives.

Figure 2. Thermally modified wood lumber

Thermal modification is a great option to increase the performance of wood and according to Wardell (2015) thermally modified wood products such as decking is very competitive in price when compared to traditional premium decking or tropical species such as Ipe, however, the current market for TM wood in the US is still hesitant to try this product. Potential consumers still know little about TW wood advantages and disadvantages and there is also concern about the potential decrease of mechanical strength (Wang et al 2012). Although there is some general knowledge that TW wood could be more resistant to water absorption and an increase resistant to decay, there is still no national and international consensus on TM wood standards (Sandberg et al., 2016 and Schnabel et al., 2007).

The basis of TM wood is the decrease in the equilibrium of moisture content and this will be affected based on the schedule (recipe) used, which includes the temperature and time of the treatment, as well as the species and type of treatment (Esteves et al., 2009). Thermally-modified wood can be produced using a closed or open drying system. During the thermal process, heat removes organic compounds and changes the cellular structure limiting the ability of the wood to absorb water (Sandberg and Kutnart 2016).

Performance metrics such as splitting, equilibrium moisture content (EMC), shrinkage and swelling, and water absorption show decreasing trends depending on the level of treatment. Other properties such as durability, surface hardness, bending, and modulus of elasticity increased on certain levels of treatment but decreased on others (Esteves et al.,2009).

Thermally-modified wood is considered a durable exterior product (Freed & Mitchell 2017). One of the main characteristics of TM wood is the removing of moisture from the wood structure, increasing the crystalline regions in the cellulose and increasing the percentage of lignin without replacing water with other chemicals. In addition to being chemical free with a profound environmental impact, TM wood is lighter than standard chemically treated products. However, is not recommended for ground contact because it does entirely remove sugars that could attract fungi or insects. In terms of appearance, the high gradual heat process creates permanent reactions in hardwood and changes the color of the wood from light to deep chocolate brown color. In many cases, the new color is a desirable aspect of wood in many potential markets (Freed & Mitchell 2017).

It is also hard for the consumers to look for an updated report with the consumption of TM wood products, where the most recent report from the volume production of TM wood is between 2012 and 2013. The Forest Products Annual Market review reported a volume of production of TM wood of 100,000 m3 (UNECE/FAO 2013). When consumers try to find specifications of different TM wood species to compare against traditional treated or non-treated similar wood products, they are unable to do so due to the lack of information and available standards., TM wood producers are in the process of trying to determine the best marketing strategies to increase market share of this material. For many TM wood producers, including the partners in this project, there a lack of information on the barriers and drivers impacting the consumption of TW wood products, which is critical to their ability to increase the use of this material .

The development of specifications sheets will be an initial step to start adapting TM wood products into the US hardwood market, which is one of the goals of this project. The methodology to develop this first phase of the project is presented on figure 1.

A set of specifications sheets will be developed with mechanical and physical performance of TM lumber using two species; yellow poplar (Liriodendron tulipifera) and red maple (Acer rubrum) from three different companies. All samples must be conditioned at 12% moisture content on a controlled temperature chamber until it reaches equilibrium.

Bibliography

Baynes, J., Herbohn, J., Gregorio, N., & Fernandez, J. (2015;2014;). How useful are small stands of low-quality timber? Small-Scale Forestry, 14(2), 193-204. doi:10.1007/s11842-014-9281-7

Boonstra, M. (2008). “A two-stage thermal modification of wood” Ph.D. Thesis in Applied Biological Sciences: Soil and Forest management. Henry Poincaré University-Nancy, France.

Buehlmann, U., Espinoza, O., Bumgardner, M., & Smith, B. (2010). Trends in the US hardwood lumber distribution industry: Changing products, customers, and services. Forest Products Journal, 60(6), 547-553. Retrieved from http://login.ezproxy.lib.vt.edu/login?url=https://search-proquest-com.ezproxy.lib.vt.edu/docview/859577129?accountid=14826

Freed, S. and Mitchell, H. 2017. Thermally modified hardwood and its role in architectural design. August. Presentation to AIA members for CEU credits.

Espinoza, O., Buehlmann, U., & Laguarda-Mallo, M. F. (2015). Thermally modified wood: marketing strategies of US producers. BioResources, 10(4), 6942-6952

Esteves, B., & Pereira, H. (2008). Wood modification by heat treatment: A review. BioResources, 4(1), 370-404.

Quesada, H.J. and R. Gazo. 2006. Mass layoffs and plant closures in the U.S. Wood products and furniture manufacturing industries. Forest Prod. J. 56(10):101-106

Sandberg, D. and Kutnar, A. 2016. Thermally modified timber: recent developments in Europe and north America. Wood and Fiber Science. Special issues for the 2015 SWST Convention. 48: 28-39

Schnabel, T., Zimmer, B., Petutschnigg, A. and Schonberger, S. 2007. An approach to classify thermally modified hardwoods by color. Forest Products Journal. 57(9):105-110.

UNECE/FAO. (2013). UNECE/FAO Forest Products Annual Market Review, United Nations Economic Commission for Europe, Food and Agriculture Organization of the United Nations, New York and Geneva

Wang, W., Cao, J., Cui, F. and Wang, X. 2012. Effect of ph. on chemical components and mechanical properties of thermally modified wood. Wood Fiber and Science 44(1): 46-53.

Wardell, C. 2015. Thermally modified decking. Professional Deck Builder. June. pp:42-44

Vertical integration is the degree to which a firm owns its upstream suppliers and its downstream buyers (Racher 2010). There are three varieties: backward (upstream) vertical integration, forward (downstream) vertical integration, and balanced (both upstream and downstream) vertical integration (Racher 2010). Vertical integration within a company can help improve its processes by having all of the steps involved of producing a product under the control of that company. For an example of balanced vertical integration, a wood products company using vertical integration would have control of harvesting the raw material from the forest, converting the logs using technologies such as debarkers, saws, presses, sanders, etc. to produce the product they are specialized for, storing said product, and eventually marketing/retailing it out. If the company just had access to the harvesting and the inputs that would be backward (upstream) vertical integration, while if it just had control of retail and distribution centers that would be considered forward (downstream) vertical integration.

The concept of vertical integration also brings about the worry of monopolizing the market since all of the process would be under one parent company. However, Richard Mpoyi (2003) suggests “So to support the competitive strength of their companies, managers that intend to change the levels of vertical integration may look at their competitors’ levels, but more importantly they should base their decisions on relevant organizational characteristics.” While certain companies may do better with a vertical integration process, not all companies need to implement it; it all depends on their structure and own company goals. The analysis showed that 50 percent of companies did not change their levels of vertical integration over the period 1980- 1997. This result suggests that once certain levels of vertical integration have been reached, these companies did not see that changing them would improve their ability to compete (Mpoyi 2003). Essentially, once a certain level of competitiveness is reached, it is not worth the time, money, and effort to keep introducing new technologies to try to keep up the vertical integration.

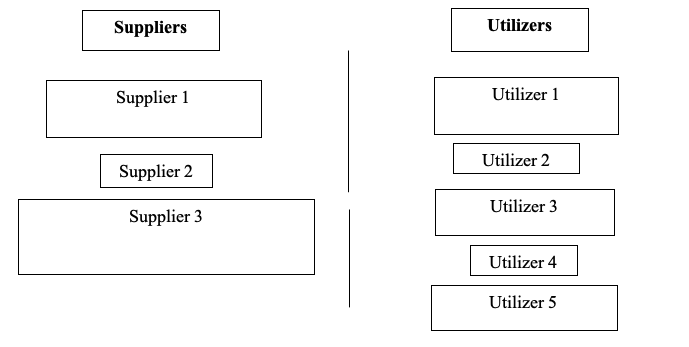

The main issue that arises with attempting to vertically integrate wood products companies is that land in the United States of America is either public or private. When establishing an integrated wood products industry around, consideration must be given to not only the quantity and quality of the wood supply, but also to the reliability of the supply over time. The best way to reduce the risk to investments associated with feedstock supply is to have a variety of land ownerships. For example, only having federal lands as a wood supply is very risky because that supply will be subject to the politics and bureaucracy associated with federal agencies (Racher 2010). Large private land parcels can lead to either investments in wood products industries not being made or those industries having the wood supply compromised by pricing (Racher 2010). Since in the USA land is split between public and private, wood products companies have issues with attempting to have a balanced vertically integrated process. This leads to most of these companies either having an upstream or downstream process, so they would have to outsource either their supply or their product. Construction companies would then have to contact multiple suppliers to try and search for the product they need for what they are building. An example of a low-scale wood products industry is represented in Figure 1 (Racher 2010).

Figure 1. Representation of small-scale wood products industry

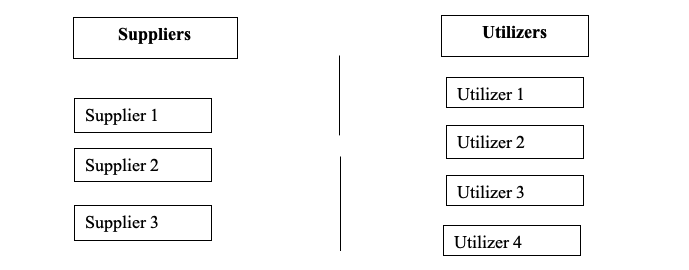

This figure would be representative of low-tech wood product industries such as firewood production and post production. As evidenced, the supplier and the utilizer side are separated, thus not using a vertically integrated system. However, since the concern of the monopolization of the market is present, having a diversity of suppliers who harvest the material to provide the raw material needed for the construction industry is ideally the most sustainable system. Figure 2 represents the idea of a balanced supplier and utilizer relationship (Racher 2010). The size of the boxes is supposed to represent the size of the supplier and utilizer.

Figure 2. Balanced wood products industry

As previously discussed, the idea of monopolization in the wood products industry is a concern, and vertical integration could be seen as an enabler of monopolization. The fact of the matter is because of the privatization of land, integrating wood products in the way of vertical integration is quite difficult. Companies either use upstream or downstream vertical integration as a way to sort of compromise this fact. The issues that construction companies face is the same sort of idea; the fact that they don’t have vertical integration in the means of they don’t have their own equipment and land to get the raw material needed to build their projects. They count on suppliers of wood products to get the material they need. Usually the process of determining a supplier is through bidding. Different factors affect the construction company’s decision of what supplier they want to proceed with. Those factors include: cost, quality, location, the relationship, and flexibility of these suppliers.

So, why is any form of vertical integration important to these wood products and construction companies? Construction companies know what they are looking for in terms of product, and having to choose a supplier through an extensive process is a burden. Most of these types of companies have downstream vertical integration where they have warehouses and distribution centers full of the material needed for their projects. Through vertical integration a firm by-passes or, more economically speaking, encompasses a market nexus (Adelman 1955). The idea of vertical integration would allow these companies to easily get to the raw material they need in a quicker time. For wood product companies, most of them have market share in the harvesting and production department (so upstream vertical integration where they have control over the production of the products needed for construction companies.). Where the wood products industry falls short, is not having their own distribution centers or retail sites, thus they would have to be a sort of middle man to the construction industry which could lead to them not getting as much of as a profit as they desire. Both of these industries coincide with each other; the wood products industry making products for the construction industry to use. If these industries can work to vertically integrate more of their processes, it would lead to an easier time of producing the product, harvesting the material they need, and selling their product.

Works Cited

Adelman, M. A. 1955. “ Concept and Statistical Measurement of Vertical Integration.” National Bureau of Economic Research. pp. 281–330.

Mpoyi,Richard. 2003. “Vertical Integration: Strategic Characteristics and Competitive Implications”. Competitiveness Review: An International Business Journal. 13(1): 44-55

Racher, Brett. 2010. “Integration of the Wood Products Industry.” Southwest Sustainable Forest Partnership. Jan.

Activity-based costing (ABC) model is a method of assigning indirect costs to products and services (Rappold, 2006). It was first introduced in the late 1970s by the Consortium for Advanced Management- International (CAM-I) (Quesada, 2010). ABC accounting model was designed to be applicable to any kind of organization regardless of product kinds, production method, and level of automation (Andersch, et.al 2014). Kaplan and Burns (1987) describe ABC model as a more appropriate method to allocate increasing overhead cost due to advancement in technology and reduced labor-intensive work, compared to traditional costing method. Because of this, the model is widely and variously used.

ABC

model is applied by obtaining the cost of each activity required to develop or

produce the final product and assigning the share of the costs to unit volume

of the product based on all processing activities. The first step in

activity-based costing involves identifying activities and classifying them

according to the cost hierarchy. Cost hierarchy is a framework that classifies

activities based on the ease with which they are traceable to a product

(Ainsworth et al, 2003). To allocate the costing in a process, traditional

costing components are divided into four different levels as unit-level costs,

batch-level costs, product-level costs, and facility-level costs (Lere 2000).

This allows high fixed overhead costs to be allocated to specific activities

that occur in the manufacturing process (Rappold, 2006). Unit level activities are activities that are

performed on each unit of product. Batch-level activities are activities that

are performed whenever a batch of the product is produced. Product-level

activities are activities that are carried out separately for each product. Facility-level

activities are activities that are carried out at the plant level. The

unit-level activities are most easily traceable to products while

facility-level activities are least traceable (Rappold, 2006).

The

main advantage of the ABC method over traditional methods is the ability to

recognize different costing activity as measures of value addition instead of only considering volume or

quantity of the product as in traditional costing practice (Rappold, 2006).

This recognition of different costing activities helps to distribute the fixed

cost evenly to each product output. The

major limitation of implementing ABC costing model in the real field is the

time and knowledge of the process and model (Lere 2000).

Howard

(1993) developed an equation to determine the variable cost of processing

individual logs into lumber which required that a variable cost function for

each machine center be calculated based upon the labor costs, maintenance

costs, and utility costs incurred at each machine center (Rappold, 2006). The

equation proposed by Howard (1993) to determine the costing of lumber from

softwood logs is:

Where,

LVC = total

variable cost for log “i”

PTIj =

processing time for log “i” at machine center “j”

MCj = variable

costs per scheduled hour for machine center “j”

m= number of

machine centers with processing time function in Group 1, used to process all

or part of the log “i”

n = total number

of machine centers used to process all or part of the log “i”

n – m = number of machine centers with

processing time functions in Group 2, used to process all or part of the log

“i”

On

this same model Howard (1993) defines the machines groups as follows; if the

processing times of individual boards or logs can be measured for activities

from any machine, they are the Group 1 machines and if it is not possible to

measure the processing times for individual product for activities from any

machine are Group 2 machines. The variable costs of the Group 1 machine centers

are measured as a function of the individual pieces. The variable costs of the

Group 2 machine centers are measured as a function of volume (Howard 1993).

Howard’s equation acknowledges that not all machine centers are uniformly utilized

when processing logs.

According

to Garrison et. al., (1999), to implement the ABC model there may be different

approach but the six core steps of costing are the major which are identified

as:

Step 1:

Identified activities are grouped together in activity pools

Step 2: Analysis

activity identifies indirect cost and assigns it to an end product

Step 3: Based on

the findings of step-1 and step-2, assign a cost to an activity pool

Step 4:

Calculate activity rates for final product

Step 5: Assign

the cost to cost objects with reference to identified activity pools and rates

Step 6: Prepare

the costing reports

Application

of ABC model to determine the hardwood and softwood CLT cost

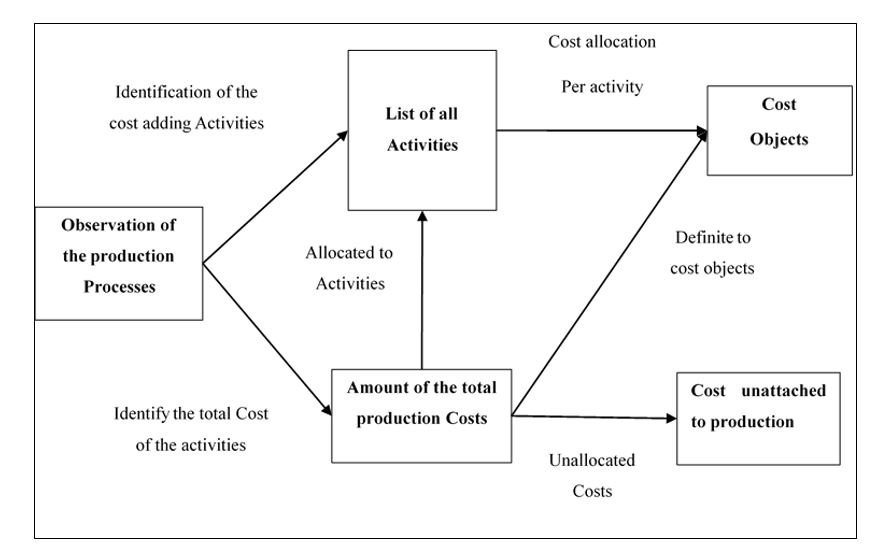

The cost of the CLT can be evaluated based on ABC model, as discuss earlier, to determine the variable cost of CLT production. The ABC model is more appropriate in this context because there will be two different products from same process that vary only in primary raw materials and each process with different raw material (may) have different functioning factor and time. To implement the ABC model, six core steps of costing implementation, as discussed by (Garrison et. Al., 1999), will be followed. The overall process of the cost evaluation is presented in Figure 1.

Figure 1: Purposed ABC model for

product costing of CLTs.

For

the cost analysis of the CLT production, all the activity that adds economic

value to the product will be identified and grouped together in activity

pools. The activity pools can be studied

as Unit level, Batch Level, and Product Level. The overall possible activities

in the process of CLT manufacturing include but not limited to:

CLT system

design cost

Raw material

acquisition cost

Direct material cost

Purchase order cost

Delivery cost

CLT processing cost

Direct labor cost

Machine setups

Operational cost

Primary planning and QC check cost

Finger jointing cost

Board cutting

Adhesive application cost

Pressing and drying cost

Trimming and edging cost

Quality test cost

CNC Processing for the architectural plans

Product packaging cost

Machine testing and calibration cost

Maintenance and cleaning cost

Transportation cost

Installation of the CLT system

Management cost

Administrative cost

Advertisement cost

Insurance/ software cost

In

the second step, the activity analysis will be performed to identify total

indirect costs for manufacturing CLT from both softwood and hardwood (SPF/SYP

and yellow poplar). Those costs will be allocated to an end product. In the

third step, the cost is allocated to an activity pool. Considering the cost of

each activity pool, activity rates for the final product are calculated in the

fourth step. Once activity costs, pools, and rates are identified and clearly

defined, the next step is to allocate cost to cost objects. With all the

information obtained, the financial report will be prepared in the final

step. The total cost of the CLT will be

the sum of the cost from production to the installation of the CLT system.

References:

Ainsworth,

P., & Deines, D. McGraw-Hill Higher Education New Product Listing: Titles

due for publication April-June 2003 BUSINESS.

Andersch,

Adrienn; Buehlmann, Urs; Palmer, Jeff; Wiedenbeck, Janice K.; Lawser, Steve.

2014. Product costing guide for wood dimension and component manufacturers.

Gen. Tech. Rep. NRS-140. Newtown Square, PA: U.S. Department of Agriculture,

Forest Service, Northern Research Station. 31 p

Garrison,

Ray H., and Eric W. Noreen. Managerial Accounting. 9th ed. Boston: Irwin

McGraw-Hill, 1999.

Howard,

A. F. (1993). A method for determining the cost of manufacturing individual

logs into lumber. Forest products journal, 43(1), 67.

Kaplan,

Robert S., and W. Bruns. 1987. Accounting and Management: A Field Study

Perspective. Boston: Harvard Business Publishing

Lere,

J.C. 2000. Activity-based costing: A powerful tool for pricing. J. Bus. Ind.

Mark. 15(1):23–33.

Quesada,

H. P. (2010). The ABCs of Cost Allocation in the Wood Products Industry:

Applications in the Furniture Industry. Blacksburg: College of Agriculture and

Life Sciences, Virginia Polytechnic Institute and State University, PUBLICATION

420-147.

Rappold,

P.M. 2006.Activity-based product costing in a hardwood sawmill through the use

of discrete-event simulation. Ph.D. dissertation, Virginia Polytechnic Inst.

and State Univ., Blacksburg, Virginia. Available at:

http://scholar.lib.vt.edu/theses/available/etd-06122006-162052/. 250 pp

Three ply cross-laminated timber (CLT) made of Yellow Poplar

By Henry Quesada

*Articled published in the Virginia Loggers Association Newsletter in August 2018.

Cross laminated timber (CLT) has been in the market

since 2000 when it was launched in Austria by a company called KHL. A CLT panel

is composed of 3, 5, or 7 layers of lumber. Each layer is glued perpendicularly

to each other. Today almost 100% of the CLT panels being produced are made from

softwood species and it is estimated that the current CLT production in Europe

is around 1 million cubic meters.

In the United States, production of CLT started about

5 years ago. There are currently three companies producing CLT panels in the

USA: DR Johnson (OR), Smartlam (MT) and Sterling (IL). DR Johnson uses Douglas

Fir (DF) as the main raw material while Smartlam uses Spruce-Pine-Fir (SPF) and

Sterling uses Southern Yellow Pine (SYP). It has been announced that over the

next two years the following 4 CLT production facilities will start production:

Katerra in Washington, a second plant by Smartlam in Maine, LignaCLT Maine, and

International Beams in Alabama. All of the upcoming facilities will be using

softwoods as raw material.

All of the US CLT current and planned producers (except

Sterling Lumber) are in compliant with the CLT standard, PRG-320. Sterling

Lumber produces CLT matts for energy projects (non-structural application) so

there is no need to follow the CLT standard.

The CLT standard, ANSI/APA PRG-320, does not admit

hardwood lumber yet; a major hurdle for hardwood lumber to become an accepted

CLT raw material. Any softwood species as described in the ALCS under PS 20

with specific gravity higher than 0.35 should be an acceptable raw material for

CLT, according to ANSI/APA PRG-320. In most of the cases, hardwood species have

higher specific gravity than softwood, so this should not be a problem. In

addition, lumber for CLT should be dried to a moisture content (MC) of 12%+-3%.

This is also not an issue for hardwood lumber as most of it is dried to 8% MC.

A key requirement for lumber going into CLT is that

the minimum thickness in the PRG-320 is 5/8. As we know, most of hardwood

lumber is produced in 4/4 thickness. In addition, the board width should exceed

its thickness by 1.5 times (in the major strength direction of the CLT panel)

and by 3.5 times in minor strength direction of the panel. Currently, most

hardwood mills produce random widths that definitely need to be sorted out to

comply with this requirement.

Glue-line performance should be considered too. Hardwood

lumber has a more complicated cellular structure than softwood lumber that

could present challenges with adhesion. For example, some hardwoods are stiffer

than softwoods and this might require additional pressure or pressing time.

Also, chemicals in the hardwood lumber could also prevent an optimal glue-line

in- between the panels.

Machining hardwood lumber is different than softwood

lumber. Because hardwoods have a different structure, there could be a need for

different tooling and energy requirements. Some hardwoods present crystals and

other hard structures that could wear tools faster than softwood lumber. These

issues ultimately will impact cost and productivity of the planer, finger

joint, and computer numerical control (CNC) equipment of the CLT production

line.

There is also the question about the supply of

hardwood lumber for CLT. A medium size CLT plant could process about 50,000

cubic meters per year which translate to roughly 21 million board feet. It is

estimated that CLT demand in the US would be very similar to Europe or around 1

million cubic meters (424 million bf). The current structure of hardwood

industry is fragmented so it would be very difficult for a major CLT plant to

establish a steady and consistent supply of hardwood lumber under these market

conditions.

Hardwood sawmills that wish to become suppliers of a

CLT panel plant must adjust their production mix. Virginia Tech researchers conducted

a mill study and determined that Yellow Poplar lumber that is NHLA graded 2

Common and lower could be sold as raw material for CLT as long as the specific

species meet the technical requirements in the PRG 320 (specific gravity,

Modulus of Elasticity, etc). Higher grades (1 Common and higher) should

continue to be sold in the appearance market as mills can get more revenue in

this market than selling it as CLT raw material. Ultimately, hardwood sawmills

would need to train their personnel to grade hardwood lumber under structural

grading rules.

Other issues that should be considered for hardwood

CLT panels is the weight of panels. It has been estimated that hardwood CLT

panels could weigh up to 30% more than softwood CLT panels. In terms of

logistics and transportation arrangements, this could increase the overall cost

and time of the projects as additional trips are required to move the completed

hardwood CLT panels to the construction site. An alternative would be produced

3 or 5 ply softwood CLT panels and add a layer of hardwoods just to meet the

weight requirement

Finally, there is also the question of sustainability.

It has been confirmed by the US Forest Service that growth of hardwood forest

doubles its harvesting rates. However, it should be considered that growing

hardwoods might take as much as double the time of growing softwood timber. In

addition, softwood timber is growing in plantations which increases the

productivity of the timber.

As we just pointed out, it seems that there are

opportunities for hardwood lumber to participate in the CLT market. However,

there are some critical hurdles that need to be resolved before this could

happen. At Virginia Tech and other universities, we continue to generate

research in technical, manufacturing, and marketing aspects of the potential

use of hardwood lumber in the CLT market. If you have questions, please let us

know at your earliest convenience.